![]()

Tax planning strategies

Tax planning strategies involve various techniques and approaches to legally minimize tax liabilities and optimize a taxpayer’s financial situation.

Here are some common tax planning strategies:

Income Deferral:

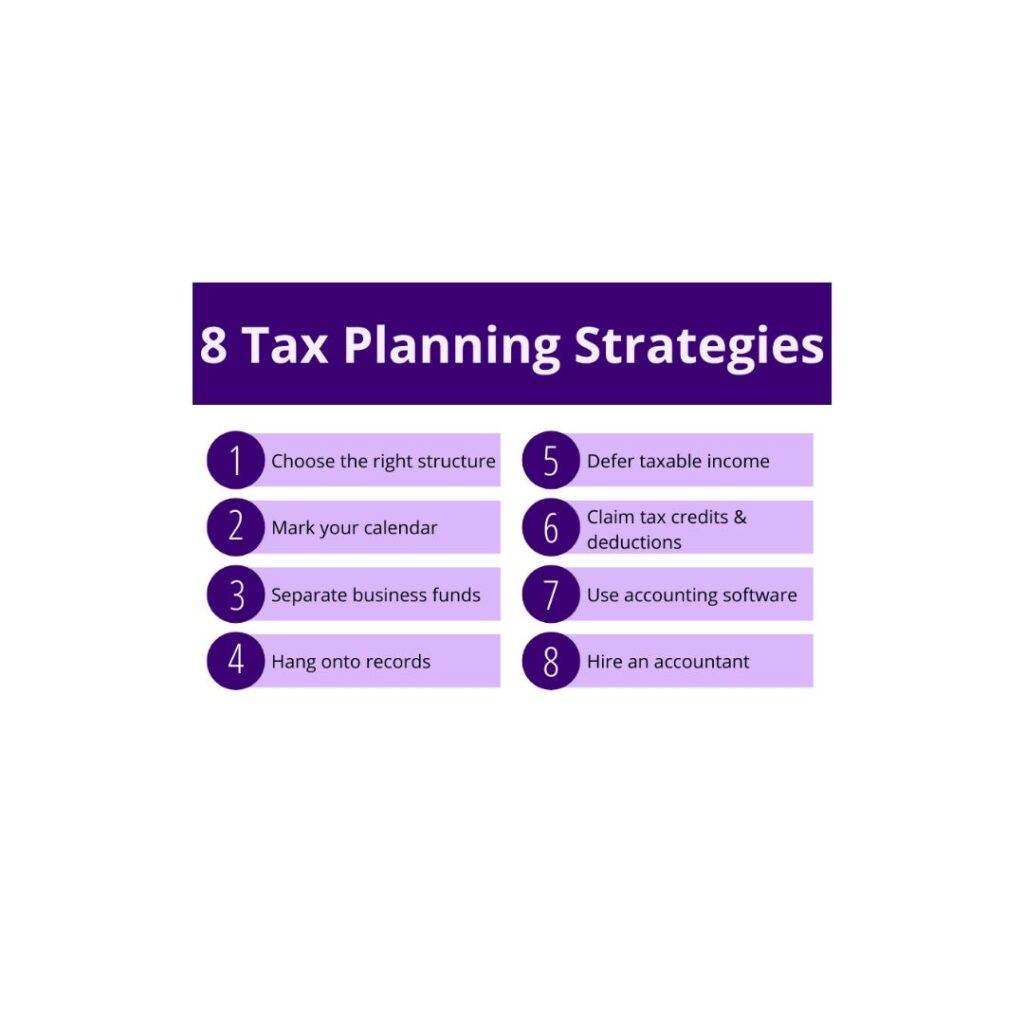

Delaying the receipt of income to a later tax year, such as deferring bonuses or income from investments, can help lower your taxable income in the current year.

Deductions and Credits:

Taking advantage of available deductions and credits, such as mortgage interest, medical expenses, education expenses, and tax credits for children or energy-efficient improvements, can reduce your taxable income or tax liability.

Retirement Contributions:

Contributing to retirement accounts, such as a 401(k) or Individual Retirement Account (IRA), can provide tax deductions and allow for tax-deferred growth of investments.

Capital Gains and Losses:

Strategically managing capital gains and losses on investments can help offset taxable gains with losses, potentially reducing the overall tax liability.

Business Expense Deductions:

Business owners can deduct legitimate business expenses, such as office rent, employee salaries, travel expenses, and equipment costs, to reduce taxable income.

Estate Planning:

Proper estate planning can help minimize estate taxes by utilizing strategies such as gifting, trusts, and establishing tax-efficient structures.

Charitable Contributions:

Donating to qualified charitable organizations can provide tax deductions, especially if you itemize deductions on your tax return.

Tax-efficient Investments:

Choosing tax-efficient investment vehicles, such as tax-free municipal bonds or tax-advantaged retirement accounts, can help reduce the impact of taxes on investment returns.

Entity Structure:

Selecting the appropriate business entity structure, such as a corporation, partnership, or limited liability company (LLC), can have tax advantages depending on the specific circumstances.

It’s important to note that tax planning strategies should be implemented in compliance with tax laws and regulations. Consultation with a qualified tax professional or financial advisor is recommended to determine the most appropriate strategies based on your specific situation and objectives.

For more information to visit:https://www.incometax.gov.in

FAQs

1.Why is tax planning important?

- It helps individuals and businesses save money, comply with tax laws, and make informed financial decisions.

3. What are some common tax planning strategies?

- Common strategies include maximizing deductions, contributing to retirement accounts, and utilizing tax credits.

4. How can retirement accounts help with tax planning?

- Contributions to retirement accounts like 401(k)s or IRAs can reduce taxable income, deferring taxes until withdrawal.

5. What are tax deductions?

- Tax deductions are expenses that can be subtracted from total income, reducing the amount of taxable income.

6. What are tax credits?

- Tax credits directly reduce the amount of tax owed, making them more valuable than deductions.

7. How does timing affect tax planning?

- The timing of income and expenses can influence tax liability; deferring income to the next year may reduce current taxes.

8. What is capital gains tax planning?

- This involves strategies to minimize taxes on profits from the sale of assets, such as holding investments longer to benefit from lower rates.

9. Can business expenses be used in tax planning?

- Yes, businesses can deduct eligible expenses, reducing taxable income and overall tax liability.

10. When should I start tax planning?

- It’s best to start tax planning early in the year to identify strategies and make adjustments before tax deadlines.

For further details access our website https://vibrantfinserv.com