![]()

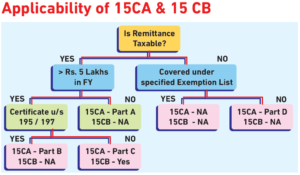

Form15CA and 15CB

Here are some instances when these certificates may not be necessary:

1.Exemptions under the Income Tax Act:

There are specific exemptions and thresholds mentioned in the Income Tax Act, where remittances may be exempt from the requirement of Exemptions from Form 15CA and 15CB.

These exemptions vary based on the nature of the transaction and the applicable provisions of the Act.

It is important to refer to the latest guidelines or consult with a tax professional to determine if an exemption applies in a particular case.

2.Lower Value Remittances:

In some cases, where the total value of the remittance does not exceed a specified threshold determined by the Indian tax authorities, the requirement for Form 15CA and Form 15CB may be waived.

The threshold amount is subject to change and should be verified based on the latest guidelines.

3.Covered under a DTAA:

If the transaction cover under a Double Taxation Avoidance Agreement (DTAA) between India and the recipient’s country, and the transaction falls within the ambit of the agreement.

The requirement for Form 15CA and Form 15CB maybe exempt or modify based on the specific provisions of the DTAA.

It is important to note that the exemptions and thresholds can change over time, and it is advisable to refer to the latest guidelines.

Consult with a qualified professional to determine whether Form 15CA and Form 15CB required for a particular transaction.

Additionally, it is important to comply with any other regulatory or reporting requirements that may be applicable to the specific type of transaction.

Such as those imposed by the Reserve Bank of India (RBI) or other authorities.

FAQs:

For further details access our website: https://vibrantfinserv.com